How to Avoid Student Loan Default: Warning Signs to Watch

The Protect Borrowers Coalition ran the math and landed on a number that deserves a moment of quiet: in 2025, a new federal student loan borrower defaulted every 9 seconds. By the time Q1 2026 closed out, the New York Fed reported 2.6 million additional defaults in a single quarter, on top of the 1 million who fell in Q4 2025. That's 3.62 million people in six months.

What makes this particularly striking is who these borrowers are. According to New York Fed data, nearly 75% of newly defaulted borrowers were current on their loans or not yet in repayment as recently as 2019. They weren't reckless. They simply faced a system that resumed demands before they were ready to meet them.

If you're carrying federal student debt right now, the warning signs that precede default are worth understanding precisely, not in the abstract.

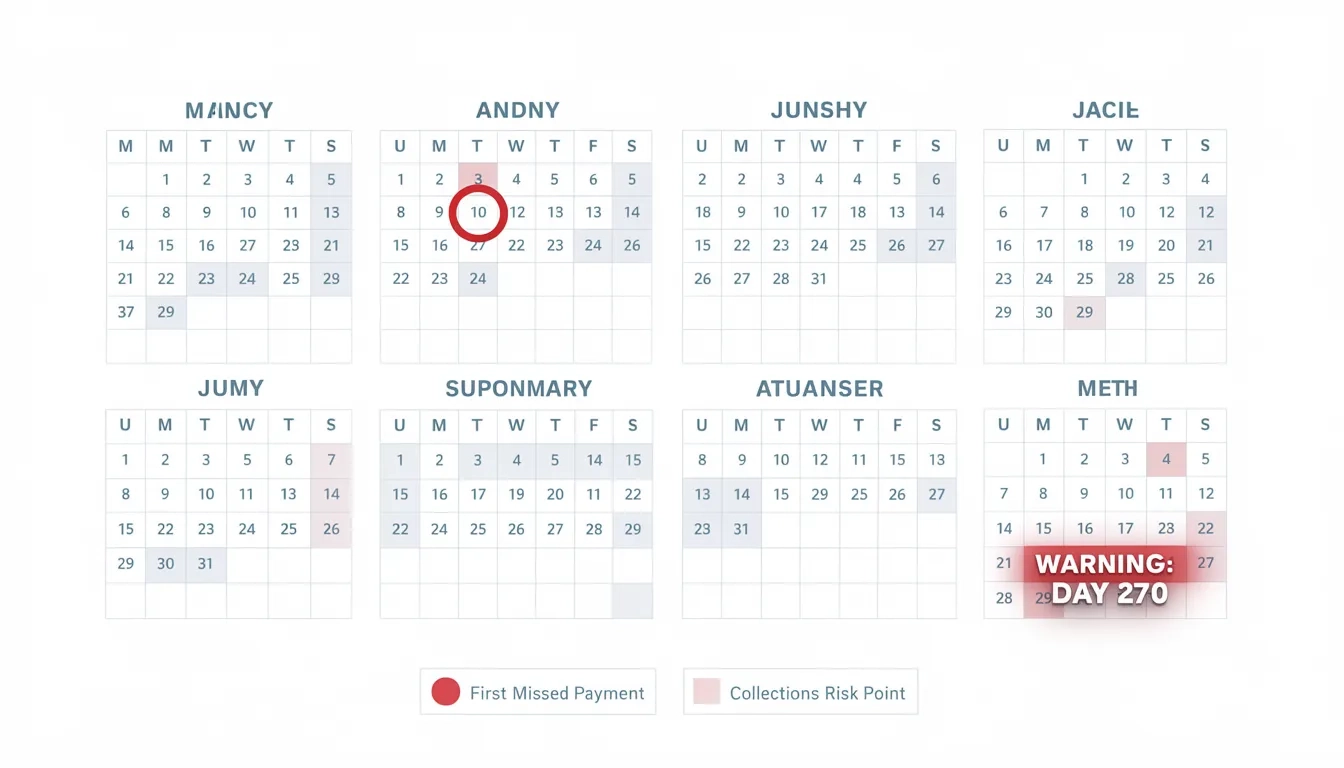

The 270-Day Clock Most Borrowers Don't Know About

Federal loans don't default on day one of a missed payment. They enter default after 270 consecutive days without payment, roughly nine months. Private loans move faster, often defaulting after 90 to 120 days depending on your lender agreement, but the federal countdown is what catches most people off guard because it feels distant until it isn't.

Here's what happens before you hit 270: at 90 days past due, your servicer reports the delinquency to Equifax, Experian, and TransUnion. Your credit score drops well before you're technically in default. Many borrowers first notice something is wrong not through a formal notice, but through a smaller-than-expected tax refund — because the Treasury Offset Program lets the government redirect federal refunds to collect on delinquent accounts before default is even official.

The nine-month window sounds like breathing room. But servicers often send notices to outdated email addresses and old mailing addresses, so the countdown runs while borrowers stay unaware. By the time the phone calls start, months have already passed.

Six Warning Signs You're Heading Toward Trouble

These are the signals that show up before default. Most articles skip straight from "what is default" to "consequences of default." The space in between is where you can actually do something.

Warning sign 1: You're paying other bills first and deprioritizing student loans.

This is the most statistically consistent precursor to default. New York Fed data from early 2026 shows that among newly defaulted student loan borrowers, 57.3% were already delinquent on credit cards and 39.8% were behind on auto loans. The student loan default didn't appear out of nowhere. It followed months of quiet triage, where borrowers paid what felt most urgent and deferred the rest.

If your student loan payment is regularly getting pushed to the bottom of your stack, that's not just a cash flow problem. It's a warning that your repayment plan no longer fits your income.

Warning sign 2: Your income dropped and you haven't told your servicer.

Job loss, reduced hours, a move to a lower-paying role — any of these can make a fixed monthly payment suddenly unworkable. The typical response is silence. Borrowers stop picking up the phone, stop opening mail, and hope the situation sorts itself out. It doesn't. But the fix is genuinely accessible: call your servicer before missing a payment, not after. Income-driven repayment plans can legally reduce your monthly payment to $0 if your income is low enough.

Warning sign 3: You don't know who your servicer is or what repayment plan you're on.

This sounds almost too basic to name. But in 2025 and 2026, with multiple large servicers transferring loan portfolios and thousands of borrowers moved off the SAVE plan after legal challenges froze it, many people genuinely don't know where their loan currently sits. Log into StudentAid.gov and check. If your servicer changed or your plan is unclear, that's worth resolving today, not when a payment fails.

Warning sign 4: You submitted an IDR application but haven't confirmed it's processing.

As of March 2026, 554,000 income-driven repayment applications were sitting in a processing backlog at the Education Department. Submitting an application does not automatically pause your payment obligations. If you applied and never received confirmation of processing or enrollment, you may be in an administrative gap — technically un-enrolled, with payments still accruing. Call your servicer and ask for your application's current status.

Warning sign 5: Your credit score is dropping sharply across multiple accounts at once.

Among borrowers who defaulted between Q3 2024 and Q4 2025, the average credit score fell 91 points (from 567 down to 476 on average). That kind of drop rarely happens because of one missed student loan payment. It happens because of cascading delinquency across credit cards, auto loans, and other obligations at the same time. A broad, fast credit score decline is a signal of systemic financial stress, and student loans are usually next in line.

Warning sign 6: You're enrolled in autopay but your bank account has insufficient funds.

Autopay is genuinely useful — servicers typically offer a 0.25% interest rate reduction for enrollment, and it removes the risk of forgetting a due date. But autopay doesn't protect you if the account it draws from goes negative. A returned payment still counts as a missed payment. Check that your autopay account has enough cushion, especially around irregular expense months.

Who Is Actually at Most Risk Right Now

The image of the struggling recent grad buried in debt is not the dominant profile of a 2026 defaulter. Newly defaulted borrowers average 38.9 years old (up from 36.4 pre-pandemic), and borrowers over 50 are defaulting at disproportionate rates. These are mid-career adults who paused payments during the pandemic-era relief period and came back to a financial landscape that had shifted around them.

Geographically, the defaults are concentrated in the South. Louisiana, Mississippi, Alabama, Georgia, and South Carolina each have more than 10% of their borrower population in default — well above the national average. Michele Zampini of the Institute for College Access and Success said it plainly: "All signs are pointing toward worse default rates than ever."

| Borrower Profile | Primary Risk Factor |

|---|---|

| SAVE plan enrollees (plan frozen) | Administrative limbo; unclear payment status |

| Mid-career borrowers (35–55) | Higher balances, less income flexibility |

| Southern-state borrowers | Highest default concentration nationally |

| Borrowers who paused during COVID | May have forgotten repayment mechanics entirely |

| Multi-servicer loan portfolios | Coordination gaps, missed communications |

My honest read on this: the administrative failures here have been substantial. Millions of people did the right things — enrolled in income-driven plans, submitted paperwork, set up autopay — and still got caught in processing backlogs and plan transitions they didn't fully understand. The blame narrative of "irresponsible borrowers" doesn't hold up against the data. Many of these defaults were preventable with better servicer communication and smoother plan transitions.

What to Do Before Day 270 Arrives

Your options shrink dramatically after default. Before that 270-day mark, federal borrowers have meaningful protections available at no cost.

Here's a practical decision framework:

- You can afford your current payment — Set up autopay, keep the account funded, and verify your servicer contact information is current.

- You can afford some payment, but not your full amount — Apply for an income-driven repayment plan immediately at StudentAid.gov. Your payment can drop to $0 based on income. This doesn't happen automatically; you have to apply.

- You can afford nothing right now — Apply for economic hardship deferment or request forbearance before missing a payment. Servicers can often grant forbearance with a single phone call.

- You've already missed payments — Call your servicer today. Ask specifically about the Fresh Start program or rehabilitation options. You have until day 270 to act before collections begin.

A few specific options worth understanding:

- Income-Driven Repayment (IDR): Ties your monthly payment to a percentage of your discretionary income. IBR, PAYE, and ICR are currently available (SAVE is partially frozen due to litigation).

- Economic Hardship Deferment: Suspends payments if you're receiving federal assistance or working full-time below 150% of the poverty line.

- Public Service Loan Forgiveness: If you work for a government agency or qualifying nonprofit (which covers more roles than most people realize), 120 qualifying payments lead to full discharge of remaining balance.

Call the number on your most recent loan statement, not a number you find through a general web search. Loan servicer scams targeting distressed borrowers have increased alongside the default surge.

What Actually Happens After Default

Being specific here matters because the consequences are unusual enough that most people don't anticipate them.

Tax refund seizure through the Treasury Offset Program happens automatically, with no court order and no advance notice (beyond a required letter that often goes to an old address). The IRS redirects your refund before it reaches you.

Wage garnishment allows the Department of Education to take up to 15% of your disposable income directly from your paycheck. Crucially, this requires no lawsuit for federal loans. Your employer gets a garnishment notice. That detail makes this consequence different from most forms of debt collection.

Social Security offset is the provision that surprises older borrowers most. The government can garnish Social Security benefits to satisfy defaulted federal student loans. Given that the average defaulted borrower is now nearly 39 years old, some of these borrowers will reach retirement age still carrying this liability.

Mortgage denial via CAIVRS. The Credit Alert Verification Reporting System is a federal database that mortgage lenders must check before approving FHA, VA, and USDA loans. A defaulted federal student loan blocks approval regardless of how good your credit score looks otherwise. Clearing CAIVRS requires rehabilitating or consolidating the defaulted loan, which takes months.

Default doesn't just damage your credit score. It reaches into your paycheck, your tax refund, your Social Security benefits, and eventually your ability to finance a home. Each consequence compounds the next in ways most borrowers don't see coming until they're already inside it.

The 91-point average credit score drop (from the NY Fed data) may understate the damage for individual borrowers, since those numbers are averages across a large population that includes borrowers who recovered partially before the Q4 2025 count.

Bottom Line

Student loan default is not a distant edge case right now. 3.62 million borrowers learned that the hard way in six months.

- Log into StudentAid.gov this week and confirm your servicer, your repayment plan, and whether any pending IDR applications are actually in process. Do not assume the status you had six months ago is still accurate.

- If you can't afford your payment, apply for IDR before missing a payment. Payments can legally drop to $0, but only after you apply. The application does not auto-protect you while it's pending.

- Watch for delinquency on other credit products. Falling behind on credit cards and auto loans at the same time as student loans is the clearest early pattern in the default data. Treat it as a signal, not a coincidence.

- The 270-day window is real, and it closes. Before default, you have options that cost nothing. After default, the government can garnish wages and tax refunds without a court order. The math on acting early is not close.

Most of this is fixable with a phone call. The harder part is making that call before the situation forces your hand.

Frequently Asked Questions

What's the difference between student loan delinquency and default?

Delinquency starts the day after you miss a payment. Default on federal loans is a specific designation that hits at 270 days past due. Credit bureaus receive delinquency reports at the 90-day mark, well before default. Default is what triggers wage garnishment and tax refund seizure.

Can I get out of student loan default after it happens?

Yes. Federal borrowers can exit through loan rehabilitation (nine on-time payments over 10 consecutive months), consolidation into a Direct Loan, or full repayment of the outstanding balance. The Fresh Start program offered an expedited pathway for some borrowers — check current eligibility at StudentAid.gov, since availability has changed as the program matures.

Myth vs. reality: Is student loan default mainly a problem for young borrowers who overspent?

The data says no. The average newly defaulted borrower in early 2026 was 38.9 years old, and 75% of them were current on their loans as recently as 2019. Many are mid-career adults caught between rising living costs, changed repayment plans, and administrative delays they didn't anticipate. Framing default as a character failure obscures what the numbers actually show.

What should I do if my IDR application is pending and my payment is coming due?

Call your servicer and request an administrative forbearance explicitly tied to the pending application. With over 554,000 applications in the queue as of March 2026, processing times are long. Forbearance prevents delinquency from accumulating while you wait, but you have to ask for it — it doesn't apply automatically just because you submitted paperwork.

How fast will my credit score drop if I miss student loan payments?

Servicers report to the three major credit bureaus at 90 days past due. From there, additional damage accrues when the default designation hits at 270 days. The borrowers in the NY Fed dataset saw an average 91-point drop between Q3 2024 and Q4 2025 — and that's an average. Some borrowers lost significantly more.

Does student loan default affect my ability to get a mortgage?

Yes, in a specific and often surprising way. Federal loan defaults are entered into the CAIVRS database (Credit Alert Verification Reporting System), which lenders are required to check before approving FHA, VA, and USDA loans. A defaulted loan in CAIVRS blocks approval regardless of other credit factors. Resolving it requires exiting default through rehabilitation or consolidation before a mortgage application can proceed.