How to Estimate Your Financial Aid Before Filing FAFSA

Most families wait until they're filling out the FAFSA to figure out what they might receive in aid. By then, the moves that could have changed that number are already off the table. The income year is locked. The assets are where they are. All you can do is fill in the boxes and hope.

The smarter approach: run the estimates months before the FAFSA opens. Free tools exist that show your likely Student Aid Index and let you model different scenarios before anything is official. You can walk into the process with a real picture of what each school on your list will actually cost — not the sticker price, but the price for your family.

The Formula Behind Every Aid Package

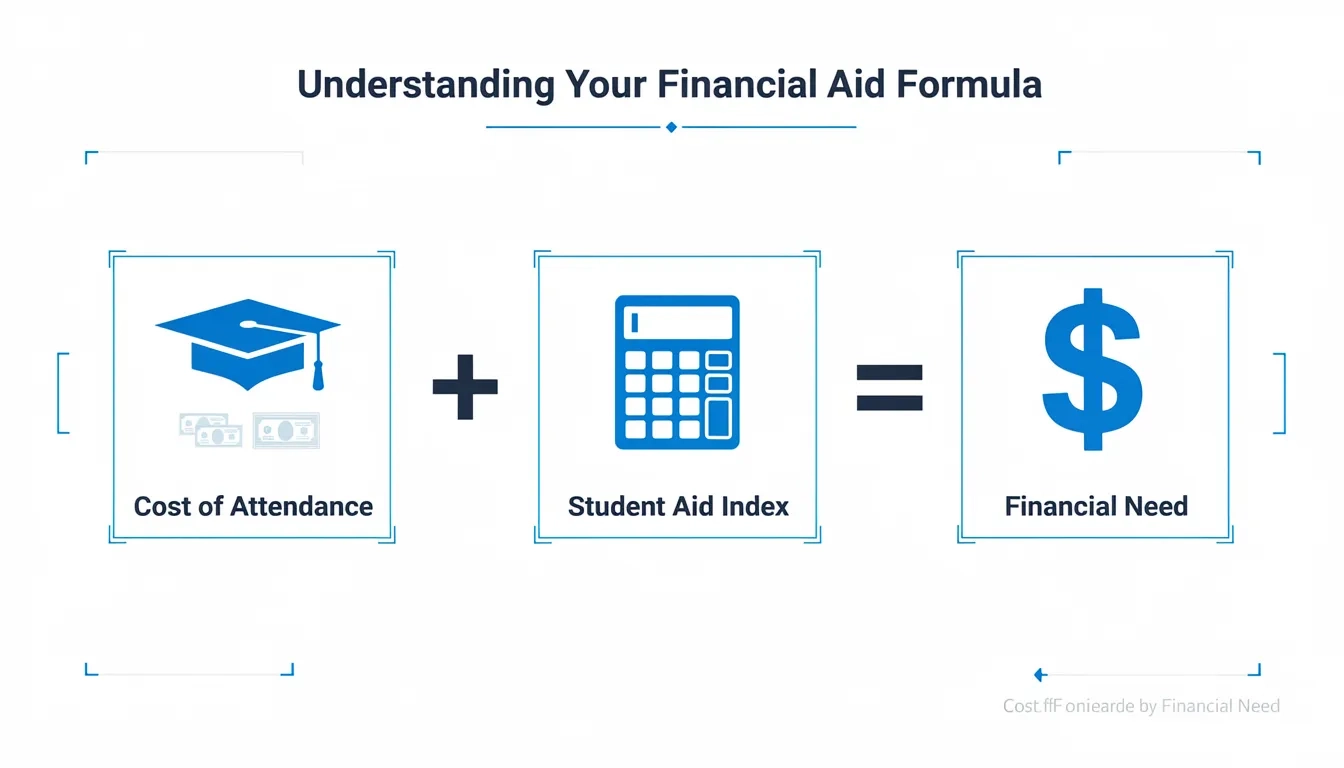

Every financial aid decision starts with the same equation:

Financial Need = Cost of Attendance (COA) minus Student Aid Index (SAI)

That's the whole thing. COA is what the school says it costs to attend for a year (tuition, room and board, books, transportation). SAI is the number the federal formula assigns to your family based on income and assets. A school with a $65,000 COA and an SAI of $12,000 would show $53,000 in financial need. That need then gets filled — partially or fully — with grants, work-study, and loans.

The SAI can range from -1,500 (maximum need) to 999,999. A negative SAI doesn't mean the school cuts you a check. It flags that your family qualifies for the most generous federal aid tier, including the full Federal Pell Grant.

Pull These Numbers Together First

Accurate inputs matter more than the tool you use. A wrong income figure can throw your estimate off by $3,000 or more.

For a dependent student, gather:

- Parent(s) Adjusted Gross Income from the 2023 federal tax return (for the 2025-26 FAFSA, the formula uses "prior-prior year" income — two years back from the award year)

- Total income taxes paid and untaxed income (401k contributions, child support received, HSA contributions)

- Parent assets: checking, savings, brokerage accounts, 529 accounts owned by a parent, rental property net worth

- Student assets: any accounts in the student's name, custodial accounts, savings bonds

- Household size

What you don't report:

- Retirement accounts (401k, IRA, pension)

- Primary home equity

- Life insurance cash value

One of the most consequential distinctions in the entire formula: parent-owned assets are assessed at roughly 5.64% per year, while student-owned assets are assessed at 20%. The same $10,000 adds about $564 to the SAI when it's in a parent savings account, or roughly $2,000 when it's in the student's name. This is why financial planners consistently recommend keeping college savings in parent-owned 529 accounts.

Tool #1: The Federal Student Aid Estimator

The U.S. Department of Education offers a free Student Aid Estimator at studentaid.gov. It mirrors the actual FAFSA questions and produces an estimated SAI using the official federal formula — not a third-party approximation.

It takes about 15 minutes with a tax return handy. At the end, you get an SAI estimate and a rough indication of Pell Grant eligibility. For 2025-26, the maximum Pell Grant is $7,395. Students with an SAI near zero qualify for the full amount; eligibility phases out as SAI climbs toward approximately $6,500. Once you're above that threshold, Pell drops to zero.

Start here. This is the baseline number every other estimate builds on.

Tool #2: Third-Party SAI Calculators for Scenario Modeling

If you want to run multiple scenarios quickly — what if parent income drops next year, or what if you pay off the car loan before filing — third-party calculators let you iterate without re-entering everything from scratch.

FinAid.org has maintained one of the most trusted SAI calculators for over two decades, updated each year when the Department of Education releases the new award year formula. Saving for College also runs a solid financial aid calculator that shows in real time how changes to income or asset values shift your SAI.

Here's a realistic example of why this matters. A family of four with $95,000 in parent AGI, $45,000 in parent savings, and a student with $3,200 in a checking account might see an SAI somewhere around $14,000 to $17,000. At a state school with a $28,000 COA, that leaves almost nothing in demonstrated need. At a selective private school with a $74,000 COA, the exact same family could qualify for $57,000 to $60,000 in need-based aid.

That's the part families miss. An expensive school can sometimes cost less than the cheap one — and you won't know until you run the actual numbers.

Tool #3: Net Price Calculators at Each School

Federal law requires every college receiving federal financial aid funds to post a net price calculator on its website. These are not generic tools. They layer that school's own grant and scholarship policies on top of the federal formula to produce an institution-specific estimate.

The difference matters. A general SAI calculator tells you what the government thinks you should pay. A net price calculator tells you what a specific school is likely to charge your family after grants, institutional scholarships, and federal aid are applied.

Brown University, Cornell, and Northeastern all maintain detailed net price calculators that also factor in academic credentials and test scores, because their merit aid formulas include those variables. Run the calculator at every school on your student's list before any application fees change hands.

Net price is the number that actually matters. Sticker price comparisons between schools are nearly meaningless — net price comparisons tell you what families in your situation actually pay.

Budget about 20 minutes per school. Running eight calculators takes an afternoon and could save you from paying application fees of $40 to $85 each at schools where the financial fit was never going to work.

Reading the Numbers: A Quick Reference

Once you have your SAI and a few net price estimates, here's a rough framework for making sense of what you're looking at:

| SAI Range | Pell Grant Eligibility | General Need Profile |

|---|---|---|

| -1,500 to 0 | Full Pell ($7,395) | Maximum federal need |

| 0 to 6,500 | Partial Pell | High need; grants likely at most schools |

| 6,500 to 20,000 | None | Moderate need; depends heavily on COA |

| 20,000 to 50,000 | None | Low need at most schools; merit aid matters more |

| 50,000+ | None | May qualify at high-COA private schools only |

One thing to know when reading any offer letter: federal loans appear in aid packages regardless of financial need. Dependent freshmen can borrow $5,500 in their first year. That's debt, not a gift, but financial aid offices bundle it in with grants — which makes offers look more generous than they are.

When comparing packages across schools, strip out the loans. Look at grant and scholarship totals only. That's your real number.

Strategic Moves That Can Shift Your SAI

Pre-filing is the window when legal, deliberate financial moves can actually change your outcome. None of this is gaming the system — it's understanding what the formula rewards.

Moves worth considering:

- Max out retirement contributions (401k, IRA, SEP-IRA) before the relevant tax year closes. These reduce your AGI and are excluded from the asset calculation entirely.

- Pay down consumer debt — credit cards, car loans, personal loans — using savings. You're converting an assessed asset (cash) into debt reduction, which lowers the asset total.

- Transfer student-owned savings into a parent-owned 529. Same money. Assessed at 5.64% instead of 20%.

- Avoid selling appreciated investments or taking IRA distributions in the income year that will appear on the FAFSA.

For the 2025-26 award year, the relevant income year is 2023. For 2026-27, it's 2024. Planning two years out gives you real flexibility. One year out still leaves meaningful options.

Mistakes That Throw Estimates Off

Using the wrong tax year. The prior-prior year rule trips up families constantly. If you input 2024 income when the formula calls for 2023 income, your estimate is wrong by definition.

Forgetting student assets. A student with $8,500 saved from summer jobs adds roughly $1,700 to the SAI. That's real, and parents often overlook it when estimating.

Ignoring the CSS Profile for selective schools. About 200 private colleges use the CSS Profile in addition to FAFSA. The CSS Profile counts home equity on your primary residence, small business value, and non-custodial parent income — assets that FAFSA entirely ignores. If selective privates are on the list, your FAFSA-based net price estimate will likely be too optimistic at those schools.

Treating net price estimates as guaranteed. Schools verify information. Some adjust merit aid after reviewing the full application. Treat net price estimates as informed projections with a margin of error of a few thousand dollars in either direction.

Bottom Line

The real financial aid planning happens before you file, not while you're filling in boxes.

- Get your baseline SAI from the federal Student Aid Estimator at studentaid.gov — this is the number everything else builds on.

- Run the net price calculator at every school on the list, even reaches and long shots. Institution-specific numbers matter; generic estimates don't.

- Model at least two scenarios in a third-party calculator: your current financial picture and one with realistic adjustments (retirement contributions, debt paydown). See how much movement is actually possible.

- Read offer letters carefully — strip out loans before comparing. Grants and scholarships are your real aid.

- If CSS Profile schools are in play, know that your FAFSA estimate won't reflect what those schools will see, and factor that in.

Frequently Asked Questions

How early should I start estimating financial aid?

Spring of junior year is the practical sweet spot. By then, you have a real college list taking shape and still have time to make strategic moves before the income year that lands on the FAFSA. The FAFSA opens October 1 of senior year — that's your hard deadline, but summer of senior year is too late for most strategic adjustments.

Does using a net price calculator share my information with the college?

No. Net price calculators are anonymous tools. No data you enter is transmitted to the admissions or financial aid office. You can run them as many times as you want, with different scenarios, and no record is created. They're research tools, not applications.

My family income is high. Should we still estimate?

Yes. A high SAI doesn't eliminate all federal options — unsubsidized loans are available regardless of income, at interest rates that beat most private alternatives. Many colleges also use FAFSA data to determine eligibility for their own institutional grants and merit awards. Not filing closes those doors entirely, and the filing itself costs nothing.

What is the student income threshold for FAFSA purposes?

For the 2025-26 formula, a student's income up to $11,770 has zero impact on the SAI. Income above that threshold is assessed at 50%. A student earning $15,000 from summer jobs and part-time work would have $3,230 above the threshold, adding roughly $1,615 to the SAI — meaningful, but not enough to make working a bad decision.

What's the difference between an SAI calculator and a net price calculator?

An SAI calculator produces a single number — your estimated Student Aid Index — based on the federal formula. A net price calculator goes further: it applies a specific school's aid policies to project your actual out-of-pocket cost at that institution. You need both. SAI shows your federal eligibility baseline; net price shows what each school will realistically charge.

Can the actual aid offer differ significantly from the net price estimate?

Yes, by a few thousand dollars in either direction. Schools that commit to meeting 100% of demonstrated need tend to produce offers close to calculator estimates. Schools with limited grant budgets, or that use a different aid model, may offer substantially less than the calculator suggested. Use the estimate as a planning range, not a guarantee.

Sources

- How Much Money Can You Get from the FAFSA in 2026? - Saving for College

- Student Aid Index (SAI) Calculator - FinAid

- Best Financial Aid and Student Loan Calculators for 2026 - Fastweb

- Student Aid Index and Pell Grant Eligibility, 2025-2026 Federal Student Aid Handbook

- 2026-27 FAFSA Student Aid Index (SAI) Calculator - College Money Method