Understanding Your Financial Aid Award Letter Line by Line

The email arrives sometime in March or April. Subject line says something like "Your Financial Aid Offer — Action Required." You click through to a portal, download a PDF, and stare at a table full of dollar amounts, acronyms, and loan types that aren't clearly labeled as loans. Somewhere in there is the number that will shape the next four years of your financial life. The letter just isn't going to hand it to you.

Here's the thing most families don't realize going in: award letters are not standardized. A 2018 New America study found colleges described the same loan types in 136 different ways across their letters. There's no federal requirement that schools format these documents consistently, so what one university calls a "Financial Aid Package" and what another calls an "Award Notice" can look completely different — even if the underlying aid amounts are nearly identical.

This guide breaks down every section so you know what you're actually looking at before May 1.

Start With Cost of Attendance — Then Get Skeptical

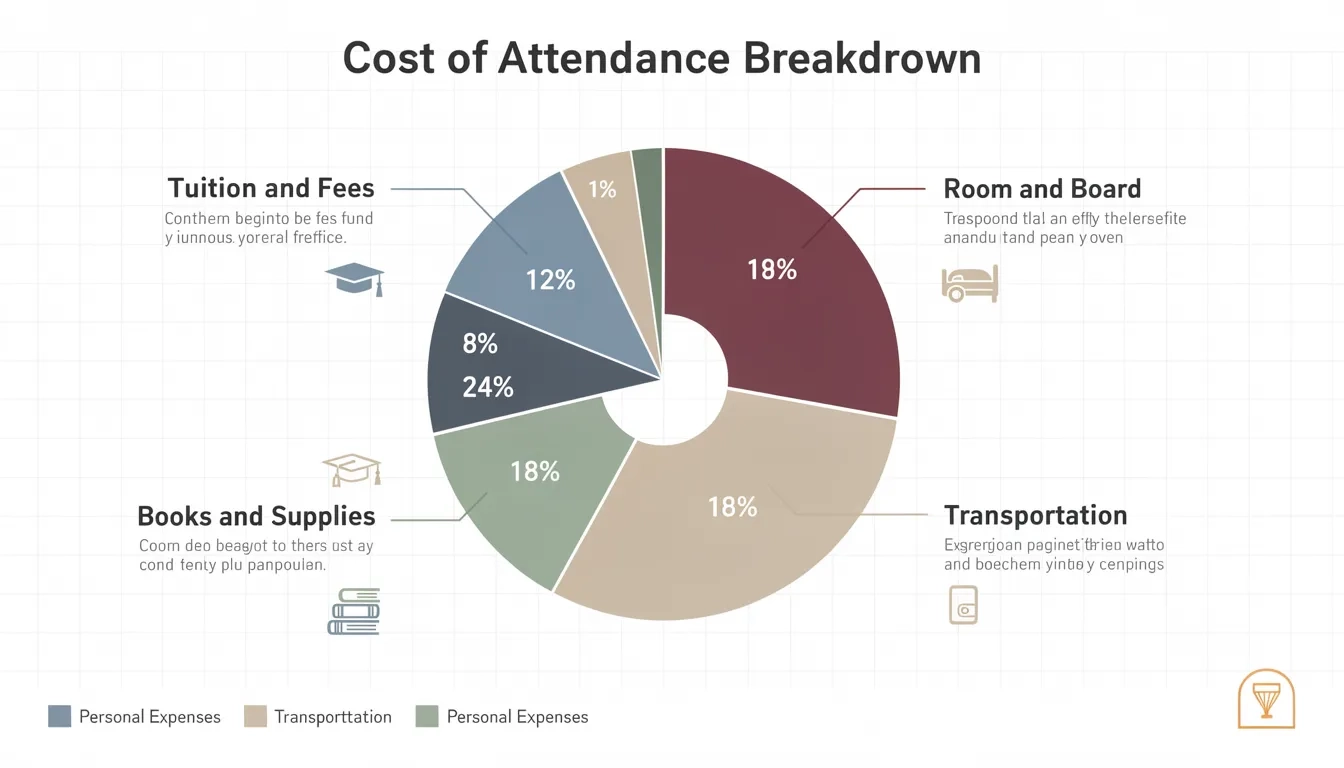

Cost of Attendance (COA) is usually the first number you'll see. It's the school's estimate of what one full academic year costs, and it covers more than tuition. A standard COA includes:

- Tuition and mandatory fees

- Room and board (or an off-campus housing allowance)

- Books and course materials

- Transportation (flights home, commuting costs)

- Personal expenses like laundry, toiletries, and incidentals

The COA matters because it's the ceiling. Your total aid package legally can't exceed it. But here's what many families miss: COA is an average estimate, not your bill. A student commuting from home pays nothing for housing. A student at a school with an open courseware program might spend $340 on books while the estimate says $1,200.

Also, COA doesn't account for annual tuition increases, which have historically run around 2% per year. A four-year degree quoted at $34,000 in year one could easily reach $36,000 by year four. Not ruinous, but worth building into any multi-year projection.

Your Student Aid Index: The Formula Behind the Offer

Near the COA, you'll typically find your Student Aid Index (SAI). This replaced the old Expected Family Contribution (EFC) starting with the 2024-25 FAFSA cycle — a significant change that expanded eligibility for many students.

The SAI is calculated by the Department of Education based on your FAFSA submission. Negative values are now possible, down to -1,500, which signals maximum financial need. The number itself isn't what you owe — it's what the formula says your family can theoretically contribute.

Two families with identical SAIs can receive very different aid packages. The school's endowment size, aid philosophy, and enrollment goals shape the offer far more than the SAI number alone does.

The Good Stuff: Grants and Scholarships

This is the section worth reading twice. Grants and scholarships are money you don't pay back, and they come from several sources:

Federal Pell Grant: The largest need-based federal grant. For 2025-26, the maximum award is $7,395. Eligibility depends on your SAI, your enrollment status, and your school's COA. Students can receive Pell funding for up to 12 semesters (roughly six years), which matters if your path to graduation isn't a straight line.

Federal SEOG Grant: Smaller amounts, up to $4,000, reserved for students with exceptional need. Not every school participates, and funds go fast — earlier FAFSA filers tend to get priority.

Institutional grants: Money from the college's own endowment. This is where the biggest variation lives. A well-funded private university can offer $45,000 or more in institutional aid; a less-endowed school might offer $4,000. These grants often carry renewal conditions — minimum GPA, continuous full-time enrollment — buried at the bottom of the letter or in a linked document.

State grants: Wildly variable. Some states run substantial programs; others barely fund anything. Check with your state's higher education agency separately.

Before you celebrate any grant number, ask one specific question: is this amount guaranteed for all four years? Many schools front-load freshman packages to look more competitive at decision time. The offer you see at 18 may not look the same at 20.

Loans: Read This Section Twice

This is where award letters cause the most damage. Schools frequently list loans alongside grants under a single "Aid Package" heading, and many families read the total and feel relieved without noticing that a significant chunk of it is borrowed money.

Student loans are aid in the sense that they're available to you. They are not aid in the sense that you eventually have to pay them back, with interest attached.

Here's how the three main federal loan types compare:

| Loan Type | Interest While Enrolled | 2025-26 Rate | Freshman Annual Limit |

|---|---|---|---|

| Direct Subsidized | Government pays it | 6.39% | Up to $3,500 |

| Direct Unsubsidized | You pay it (accrues daily) | 6.39% | $5,500 total ($2,000 unsubsidized portion) |

| Parent PLUS | Parent pays it, immediately | 9.08% | Up to COA minus other aid |

Subsidized loans are the better deal. The federal government covers interest while you're enrolled at least half-time, and for six months after graduation. You leave school with the same principal you borrowed.

Unsubsidized loans start accumulating interest on day one. A $2,000 unsubsidized loan taken out in freshman year at 6.39% will have accrued approximately $623 in interest by the time you hit the six-month post-graduation grace period, assuming a four-year program. That's money you didn't technically borrow but now owe.

Parent PLUS Loans get their own mention because some schools include them in student packages as if they're part of your offer. They're not — a PLUS Loan belongs to your parent, requires a credit check, and carries a 9.08% interest rate plus a 4.228% origination fee. If you see one in your letter, do not count it as aid you're receiving.

Work-Study: Potential, Not a Promise

Federal Work-Study (FWS) appears as a dollar amount on most award letters, and it's easy to mistake it for a tuition credit heading toward your bill. It isn't.

Work-study is an earnings opportunity. If your letter lists $2,500 in Federal Work-Study, that means you're eligible to work a part-time job (usually on campus, sometimes at approved nonprofits) and earn up to that amount. The money goes into a paycheck. You decide whether to apply it toward tuition, rent, or savings. It never hits your student account automatically.

Typical work-study jobs run 5-10 hours per week at minimum wage or modestly above. Not every student who qualifies actually finds a position, and some students find jobs but earn less than their award amount. When you're calculating costs, treat work-study as a best-case scenario rather than a guaranteed reduction.

The Number That Actually Matters: Your Net Price

Once you've gone through the full letter, you need one clean calculation.

Net Price = Cost of Attendance minus Grants and Scholarships only.

Stop there. Do not subtract loans. Do not subtract work-study. Those are either money you'll repay or money you haven't earned yet.

Here's what that looks like with real numbers:

| Item | Amount |

|---|---|

| Cost of Attendance | $52,000 |

| Federal Pell Grant | $4,200 |

| Institutional Grant | $18,000 |

| Net Price (grants only) | $29,800 |

| Subsidized Loan offered | $3,500 |

| Unsubsidized Loan offered | $2,000 |

| Work-Study offered | $2,500 |

| Remaining gap after all aid | $21,800 |

That $21,800 is the number you're actually problem-solving around. The letter won't tell you this cleanly — most letters don't even use the word "gap." That omission is, frankly, a design problem. Families deserve to see the funding gap printed in plain language, and most schools choose not to show it.

Red Flags and When to Push Back

A few things worth flagging in any letter you receive:

- Vague loan descriptions without specifying subsidized or unsubsidized status — call and ask, because the difference in interest cost over four years is real

- Front-loaded grants that don't specify renewal amounts or GPA requirements

- Inflated COA estimates, particularly in personal expense or transportation categories — you can request a breakdown

- Parent PLUS Loans listed within the student package as if they're your aid

And if the numbers don't work, appeal. The financial aid office is not the final word. If your family experienced a job loss, significant medical expense, or any income change since filing your FAFSA, you can formally request a Professional Judgment Review. Aid administrators have real discretion to adjust packages. Most families don't know to ask.

If a competing school offered substantially better aid, many schools will look at that too. Bring the competing offer, make your case calmly, and ask if the package can be reconsidered. That's not gaming the system — it's how college enrollment actually works.

Bottom Line

- Calculate your real net price by subtracting only grants and scholarships from COA. Loans reduce the upfront bill but not the eventual cost.

- Know your loan types. Subsidized is better than unsubsidized. Parent PLUS is your parent's debt, not yours, regardless of where it appears on the letter.

- Ask explicitly whether institutional grants are renewable and under what conditions.

- Treat work-study as potential income, not guaranteed aid.

- If your family's circumstances changed or you have a better competing offer, contact the financial aid office and ask for a review. They have more flexibility than the letter implies.

The award letter is a starting point, not a final answer. Treat it accordingly.

Frequently Asked Questions

Is the financial aid award letter the same as my acceptance letter?

No — they're two separate documents. Your acceptance letter confirms admission; your award letter details the financial aid offer. Many schools send them around the same time, but some send the award letter weeks after the acceptance decision. You should have both before making any enrollment deposit or committing funds.

My letter shows a large "total aid" number. Why doesn't it match what I owe?

Because that total almost certainly includes loans. When you subtract only grants and scholarships from the COA (not loans, not work-study), you get your true net price. The gap between that net price and what loans might cover is what you'll need to fund from savings, income, or other sources.

Myth vs. reality: does a higher-sticker-price school always cost more?

Not necessarily — this is one of the most expensive misconceptions in college planning. A school with a $62,000 COA that offers $44,000 in grants can cost less than a school with a $38,000 COA that offers $10,000 in grants. Six in ten families report ruling out schools based on sticker price alone, which means many students never see the actual aid offer from schools that might have been affordable.

Can I lose my institutional grant after freshman year?

Yes. Most institutional grants come with conditions: a minimum GPA (commonly 2.5 to 3.2 depending on the award), continuous full-time enrollment, and sometimes a declared major. Some schools also front-load freshman packages and quietly reduce grants in subsequent years. Ask the financial aid office directly: "What will this grant be in years two through four if my financial situation stays the same?"

What if my family's finances changed after we filed the FAFSA?

Request a Professional Judgment Review from the financial aid office. This formal process lets an aid administrator use discretion to adjust your package based on documented circumstances — job loss, divorce, significant medical expenses, a one-time income spike from selling assets. Bring documentation and make the request in writing. Schools handle these regularly and won't penalize you for asking.

Should I accept every loan listed in my award letter?

No. Accept grants and scholarships immediately. For loans, accept only what you genuinely need. You're not required to take the full amount offered, and you can usually specify a lower amount when you accept through the student portal. Every dollar you don't borrow now is a dollar you don't pay back with six-plus years of interest attached.